CATEGORY

Real Estate

Starlight Global Real Estate Fund

Seeks income and long-term growth by investing in high-quality real estate assets in markets with strong fundamentals, including growing populations and limited new supply.

Starlight Capital Advantage:

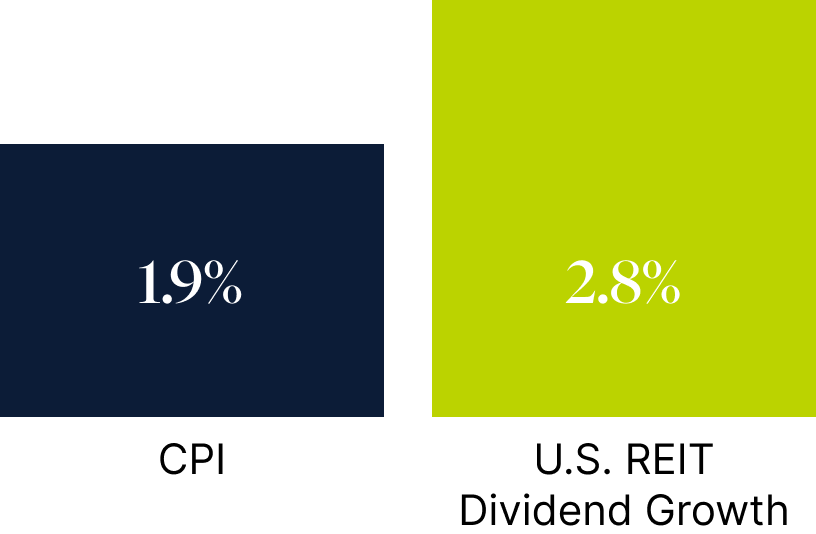

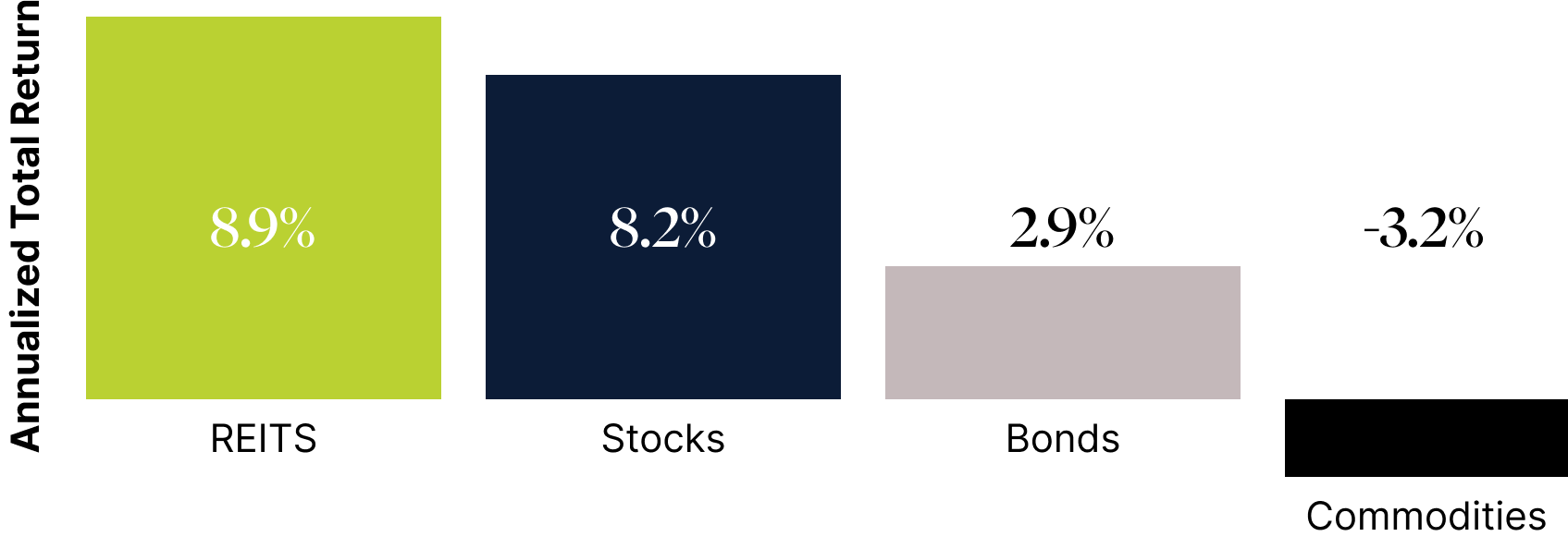

We focus on supply-constrained markets that allow real estate companies to benefit from high occupancy, rising rents and growing distributions.

This disciplined strategy positions Starlight as a leader in the real estate investment landscape, focused on robust performance for our clients.

We focus on supply-constrained markets that allow real estate companies to benefit from high occupancy, rising rents and growing distributions.

This disciplined strategy positions Starlight as a leader in the real estate investment landscape, focused on robust performance for our clients.

CATEGORY

Infrastructure

Starlight Global Infrastructure Fund

Seeks income and long-term growth by investing in high-quality businesses that provide essential services to large populations in supply-constrained markets.

Starlight Capital Advantage:

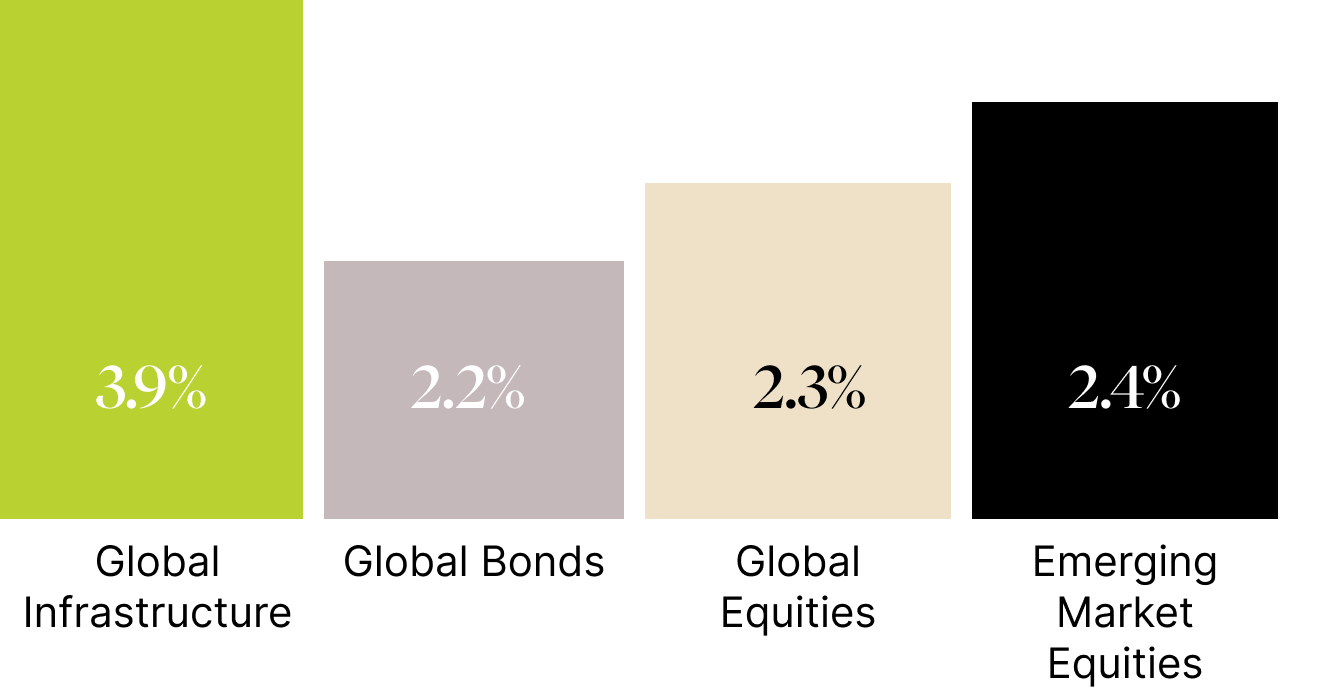

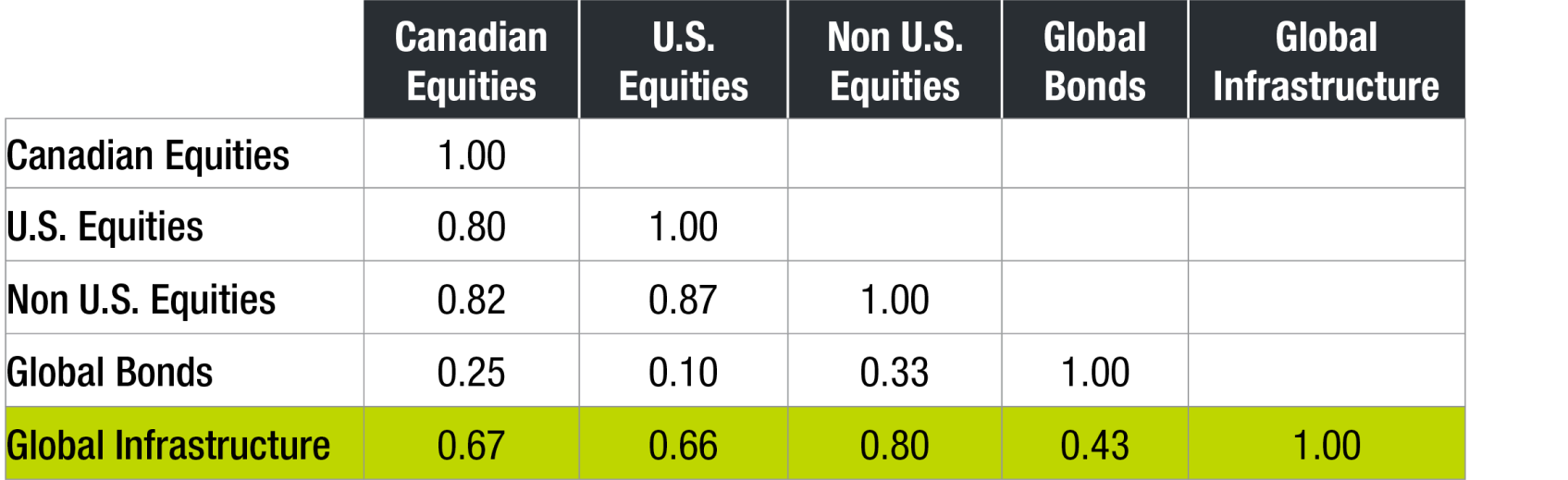

We focus on markets that support infrastructure development and renewal that allow infrastructure companies to benefit from high utilization, rising tolls and fees and growing distributions.

This disciplined strategy positions Starlight as a leader in the infrastructure investment landscape, focused on robust performance for our clients.

We focus on markets that support infrastructure development and renewal that allow infrastructure companies to benefit from high utilization, rising tolls and fees and growing distributions.

This disciplined strategy positions Starlight as a leader in the infrastructure investment landscape, focused on robust performance for our clients.